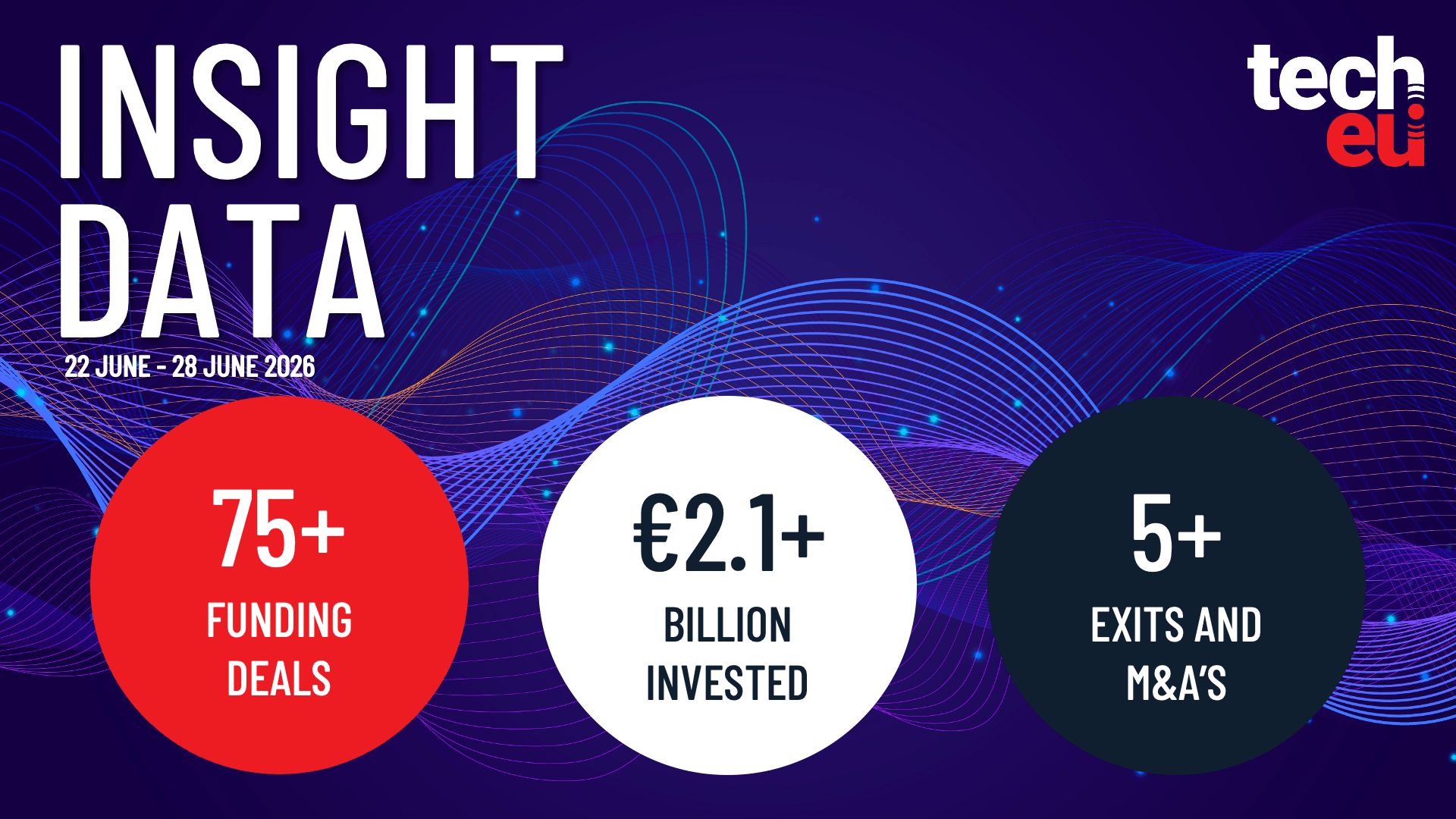

Last week, the European tech scene recorded over 75 funding rounds totalling €2.1 billion. Fintech led the sectoral ranking with €502.9 million, followed by security at €500 million and semiconductors at €349.7 million. At country level, Germany topped the list with €806.8 million, ahead of France (€625.2 million) and the Netherlands (€372.7 million).

Among the most significant deals, German Stark raised €500 million in fintech and France’s Alan secured €480 million for health insurance. But for those building or managing AI infrastructure, the Dutch chip-equipment maker Nearfield Instruments’ $380 million funding stands out. At a time when semiconductor supply chains are strained and lead times for GPUs and accelerators remain long, every investment in chip manufacturing capacity shifts the upstream dynamics of hardware stacks. Without advanced silicon, on-premise deployment of Large Language Models – even with inference configurations optimized through quantization – stays bound to chip availability.

The semiconductor battleground

Nearfield’s funding is not the only signal: the week also saw a €17 million round for France’s AlpSemi, which works on solid-state circuit breakers, and a capital injection for Germany’s Kyrok (€3.1 million), applying AI to chemical and pharmaceutical supply chains – sectors where sensors and edge computing are increasingly relevant. The piling up of capital in the semiconductor segment hints that Europe is trying to strengthen its autonomy in critical components – a theme that directly concerns technological sovereignty and GDPR compliance when data cannot leave the corporate perimeter. For CTOs evaluating self-hosted architectures, the health of Europe’s chip supply chain is a parameter to watch when calculating the Total Cost of Ownership of a training or inference cluster.

Platforms to navigate: the Funding Explorer

Tech.eu launched the Funding Explorer, now free and open to everyone during the beta phase. The platform aggregates data on rounds, company profiles, investor activity and market trends. For teams working on on-premise stacks, such tools can help map the evolving landscape of startups developing hardware components, orchestration software or security solutions for air-gapped environments. Visibility into capital flows allows one to anticipate which technologies might become mature for enterprise adoption, reducing the risk of betting on projects still far from production stability.

Beyond the numbers: on-premise in a growing ecosystem

The presence of a €500 million round in security (details undisclosed) and multiple operations in supply-chain software and industrial AI signals that the ecosystem is funding both the application layer and the foundations. Those choosing to keep models in-house, perhaps on bare-metal nodes orchestrated via Kubernetes, can benefit from this ferment because it generates European alternatives to dominant vendors, boosting competition on price and support. VRAM and memory bandwidth constraints remain dictated by accelerator availability, but innovation in scheduling and optimization tools – like those pursued by startups funded this week – can improve efficiency even on not-quite-latest hardware.

The week confirms that European tech is not only about apps and cloud services: the push on semiconductors and security creates the conditions for a more robust ecosystem for on-premise operators. Whether these investments will turn into tangible products shortening GPU wait times remains to be seen, but the signal is clear: capital is flowing where needed to reduce external dependency.

💬 Comments (0)

🔒 Log in or register to comment on articles.

No comments yet. Be the first to comment!