The Gigawatt Arbitrage—Is Elon Musk’s Data Center Strategy a 'Chess Master' Hit?

By the AI-Radar Investigative Desk | June 2026

Elon Musk isn’t playing 4D chess. Mostly because he thinks chess is a fundamentally flawed game.

Whenever tech analysts observe the world's first trillionaire making massive, seemingly coordinated market moves, they inevitably reach for the "chess grandmaster" metaphor. But to understand Musk’s latest blitzkrieg across artificial intelligence, cloud infrastructure, and the aerospace sector, we have to discard the chessboard.

Musk has publicly complained that chess is "too simple," lamenting that it features a mere 64 squares, no "fog of war," no technology tree, and "exact same pieces". While cynics note this disdain might stem from repeatedly losing to his former PayPal co-founder—and USCF Chess Master—Peter Thiel, Musk's business philosophy actually mirrors asymmetric resource games like The Battle of Polytopia.

In 2026, his strategy isn't about calculating ten moves ahead in an open-information environment. It is about brute-force resource acquisition, compressing timelines, buying structural advantages, and capturing key choke points.

Let's investigate the latest moves in the Musk empire—from the historic SpaceX IPO to his massive cloud leases with Google and Anthropic, his staggering $60 billion acquisition of Cursor AI, and what this means for the future of on-premise LLM infrastructure.

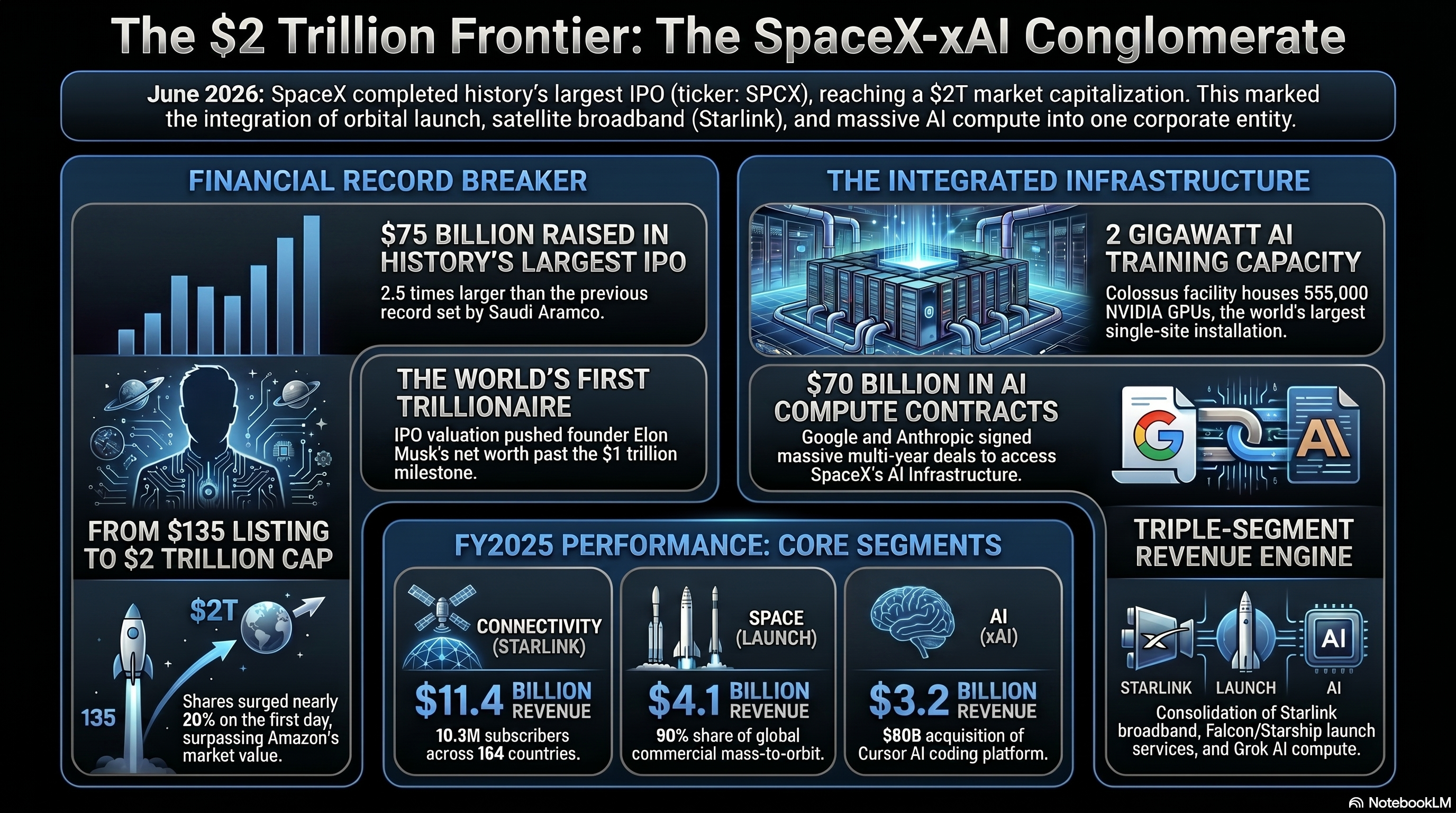

The SpaceX IPO: Funding the Polytopian Empire

To understand the scale of Musk's data center ambitions, one must look at his checkbook: SpaceX. On June 12, 2026, SpaceX debuted on the Nasdaq under the ticker SPCX in the largest initial public offering in history. Selling 555.6 million shares at a fixed price of $135, the IPO raised $75 billion and instantly valued the company at $1.77 trillion. By the end of its first trading day, shares surged past $161, pushing the market cap above $2 trillion and officially minting Musk as the world's first trillionaire.

However, the S-1 prospectus revealed a stark financial reality about Musk’s AI ambitions. Thanks to the retroactive consolidation of xAI and X into SpaceX, we learned that the company is effectively three distinct entities with highly divergent risk profiles:

Connectivity (Starlink): The profit engine. Generated $11.4 billion in 2025 revenue with $4.4 billion in operating income.Space (Launch Services): The foundation. Generated $4.1 billion in 2025, operating at a deliberate $657 million loss primarily to fund the $3 billion R&D required for the Starship program.AI (xAI, Grok, X): The cash incinerator. Brought in $3.2 billion but posted a staggering $6.4 billion operating loss.

xAI alone burned 2.5*billioninQ12026∗∗.Tobuildthe"Colossus"supercomputerinMemphis,Tennessee—amassive2−gigawatt(GW)complexthataimstohouseover555,000NVIDIAGPUs—SpaceXdirecte*d6112.7 billion) straight into AI infrastructure.

The Gigawatt Arbitrage: The Google & Anthropic Deals

If building a 2 GW supercomputer with a private natural gas power plant is the sword, how is Musk paying for the shield? Enter the "Gigawatt Arbitrage."

To offset the crushing capital burn of Colossus, SpaceX has effectively become a hyperscale landlord to its biggest competitors. Ahead of the IPO, SpaceX secured massive wholesale cloud leasing agreements with Google and Anthropic, estimated to generate $26 billion annually.

Competitive Infrastructure Agreements (2026)

| Counterparty | Monthly Lease Fee | GPU Allocation | Target Infrastructure | Contract Duration | Termination Clause |

|---|---|---|---|---|---|

| Anthropic | $1.25 Billion | 220,000+ NVIDIA GPUs | Colossus 1 (Memphis) | May 2026 – May 2029 | 90-days notice |

| $920 Million | 110,000 NVIDIA GPUs | Colossus 2 / Edge | Oct 2026 – Jun 2029 | 90-days notice |

This is the true "Chess Master" hit—even if Musk hates the game. By leasing compute to the creators of Claude and Gemini, SpaceX uses competitor capital to subsidize its own infrastructure buildout. More importantly, both contracts feature a 90-day termination clause. SpaceX retains the ultimate call option: if its internal models (like Grok) require massive, immediate scaling, Musk can simply evict Google and Anthropic and reclaim up to 330,000 GPUs without waiting years for new data centers to be built.

The Missing Link: Buying Cursor AI for $60 Billion

Infrastructure without distribution is just an expensive heater. While xAI had the brute compute and the Grok foundation model, it lacked an enterprise application layer that developers actually wanted to use.

To fix this, SpaceX executed a blockbuster $60 billion all-stock acquisition of Anysphere, the parent company of the AI coding assistant Cursor.

Used by over 7 million software developers, Cursor championed the "vibe coding" trend, allowing engineers to autonomously generate and debug software via natural language. This acquisition solves xAI's coding gap instantly. Furthermore, it gives SpaceX invaluable developer interaction telemetry. According to recent data, 81% of AI-generated code accepted by Cursor users remains in the project after one hour, proving its high utility in enterprise environments.

By bringing Cursor in-house, Musk transitions xAI from a high-loss research bet into a product generating over $2.6 billion in annualized B2B revenue.

The Consequence: The Future of On-Premise LLMs

While Musk is building centralized 2 GW monoliths, the rest of the enterprise world is quietly moving in the opposite direction.

In 2026, global enterprises are realizing that renting intelligence via public Cloud APIs (Model-as-a-Service) is an economic and security trap. Token costs are unpredictable, and feeding proprietary corporate data into public APIs represents a massive compliance risk.

The industry standard has now shifted to the "Hybrid LLM Architecture". Under this model, enterprises route 80% of their routine, sensitive tasks to highly optimized, compact open-weight models (like 7B to 13B parameter architectures) hosted entirely on-premise or in private colocation data centers. Only 20% of tasks requiring extreme complex reasoning are routed to external cloud APIs.

The financial math is staggering. Running an open-weight model on private hardware is up to 18x cheaper per million tokens than premium public APIs. For an enterprise processing millions of queries, a $120,000 capital expenditure in local GPU servers pays for itself in roughly 3.6 to 4 months. After this breakeven point, the operational cost drops to mere electricity and cooling (about $1.60 per 1M tokens vs. $30.00 in the cloud).

As data sovereignty laws tighten globally, on-premise AI deployments are transitioning from a luxury for tech giants into a baseline requirement for mid-size enterprises.

Conclusion: Reaching for the Stars (and the Sun)

Is Musk’s strategy a flawless victory? The market is pricing SPCX at 94 times its 2025 revenue, leaving zero margin for error. If Starlink growth stalls, or if xAI fails to catch up to OpenAI despite the Cursor acquisition, the massive debt and $6.4 billion AI burn rate will weigh heavily on the newly public company.

However, Musk's ultimate endgame transcends terrestrial real estate. Earth's power grid is already buckling under the weight of AI data centers. SpaceX’s long-term roadmap envisions "Orbital AI"—launching 100 gigawatts of compute capacity into Sun-synchronous orbit beginning in 2028. By using Starship to launch data centers into space, SpaceX aims to harvest limitless solar energy and utilize the vacuum of space for free radiative cooling, completely bypassing Earth's power constraints.

Elon Musk doesn't play chess. He is playing a game of cosmic resource accumulation—and right now, he owns the rockets, the satellites, the supercomputers, and the code. The rest of the tech industry is just paying him rent.

💬 Comments (0)

🔒 Log in or register to comment on articles.

No comments yet. Be the first to comment!