The latest Taiwan AI server tracker puts a figure at the top of the chart that few would expect: in June, the fastest revenue growth did not come from GPUs, network cards, or memory modules, but from rail kits and chassis. In plain English, that’s the sliding rails and metal enclosures used to mount servers inside a rack. The lead may sound mundane, but behind it lies a structural signal worth reading carefully.

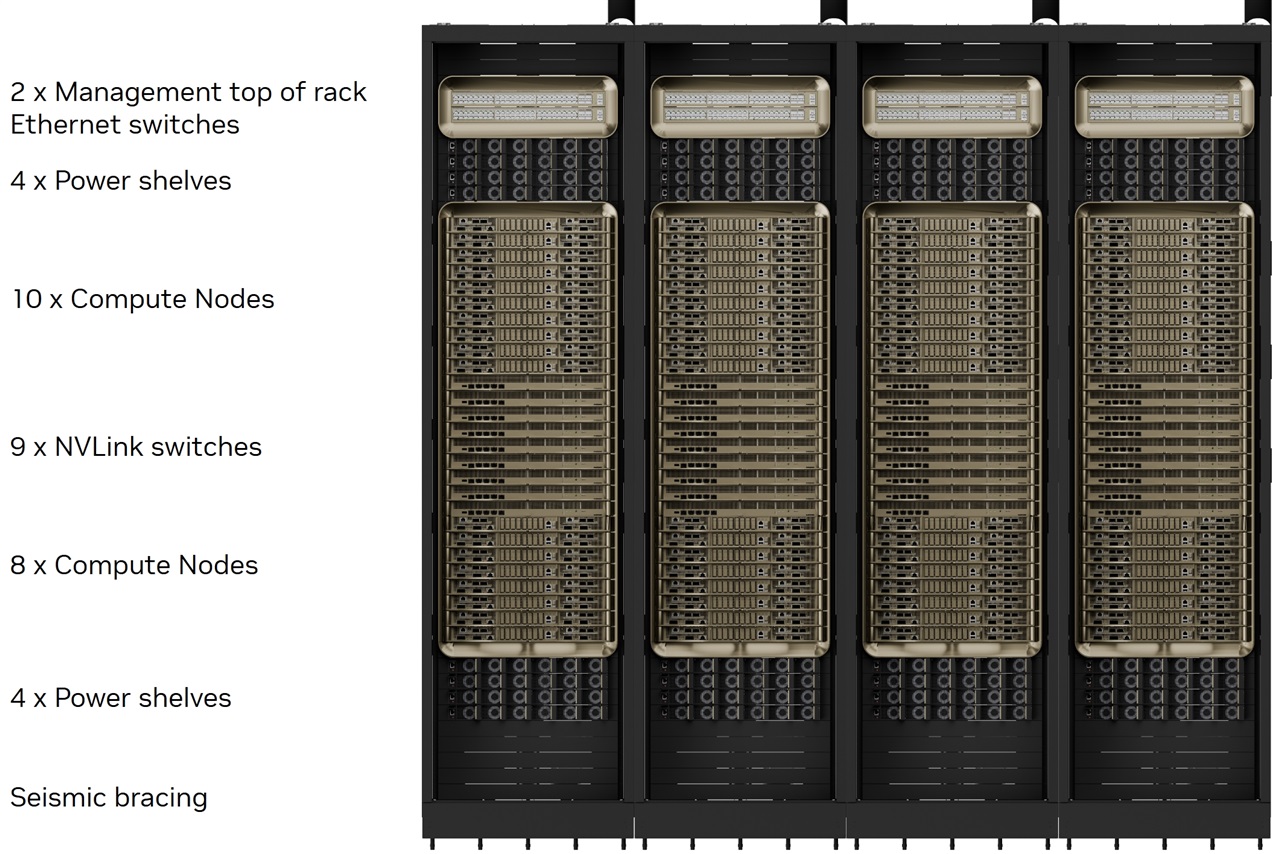

Anyone who assembles data centers knows that without rail kits, servers weighing dozens of kilos cannot be safely installed — or worse, they fall — and that a well-designed chassis is not just a container but the prerequisite for managing the power density and airflow that AI workloads push to thermal limits. The news makes sense when paired with the name cited in the source: Nvidia GB200 NVL72, a rack-scale system packing 72 GPUs into a full cabinet, weighing over a metric ton, and imposing unprecedented physical constraints on installers.

The point is not that screws and sheet metal matter more than silicon. It is that the market is sending a clear message: the AI race has moved past the phase where it was enough to add GPUs to a standard server. Today, designing an on-premise LLM infrastructure means reckoning with the entire physical stack, from connectors to reinforced floors. Taiwan’s numbers indicate that demand for these “humble” components is exploding just as NVL72 rack shipments begin to approach, and that the manufacturers — often mid-sized firms in the Taiwanese ecosystem — are enjoying margins and volumes that put them at the head of the class.

There is a second-order reading: for years, the cost of an AI server was identified almost exclusively with the price of GPUs. The sudden acceleration in rail kit revenue suggests that the TCO of an on-premise deployment is starting to absorb previously overlooked line items — not just power and cooling, but the whole mechanical bill necessary to make a converged system like the GB200 operational. In an on-premise scenario, where the organization shoulders the entire logistics and maintenance chain, underestimating these elements can turn a local inference project into an unplanned construction site.

AI-RADAR has charted frameworks for assessing on-premise deployment trade-offs, and this news adds a practical piece: ignoring rack mechanics means exposing yourself to bottlenecks that synthetic GPU benchmarks simply cannot capture. It’s not just about compute power, but about managing space, weight, and assembly logistics. For an enterprise bringing LLMs within its own walls, the choice of hardware partner cannot stop at the chip’s spec sheet.

Looking further out, the chassis-and-rail-kit story illustrates how AI hardware is evolving toward vertically integrated systems. Mechanical component suppliers, long dismissed as low-value commodities, are becoming critical nodes in a supply chain that Nvidia itself has rendered more complex and interdependent by shifting to rack-scale architectures. Whereas before a server could be assembled from interchangeable parts, an NVL72 is a semi-finished object that arrives already populated and tested: any delay in producing a chassis or a rail kit halts the entire rack delivery. Who wins? Those Taiwanese manufacturers that invested in mechanical tolerances and integration capabilities, often the very same firms already supplying the large cloud providers. Who loses? System integrators still thinking in terms of individual nodes, and anyone planning an AI data center budget by looking only at GPU prices.

In many ways, Taiwan’s tracker acts as a litmus test: when the most prosaic components become the bottleneck, the entire market has entered a maturity phase where execution excellence counts as much as chip innovation.

💬 Comments (0)

🔒 Log in or register to comment on articles.

No comments yet. Be the first to comment!