Taiwan remains the gravitational center of semiconductor packaging and testing. In June, the OSAT (Outsourced Semiconductor Assembly and Test) sector recorded a 23.7% year-over-year growth — a figure that confirms the race for production capacity, fueled by demand for advanced chips used in data centers and AI. But the charts released by Digitimes don't just highlight the usual suspects: a smaller player is capturing the spotlight, hinting at potential shifts in an ecosystem long dominated by a handful of giants.

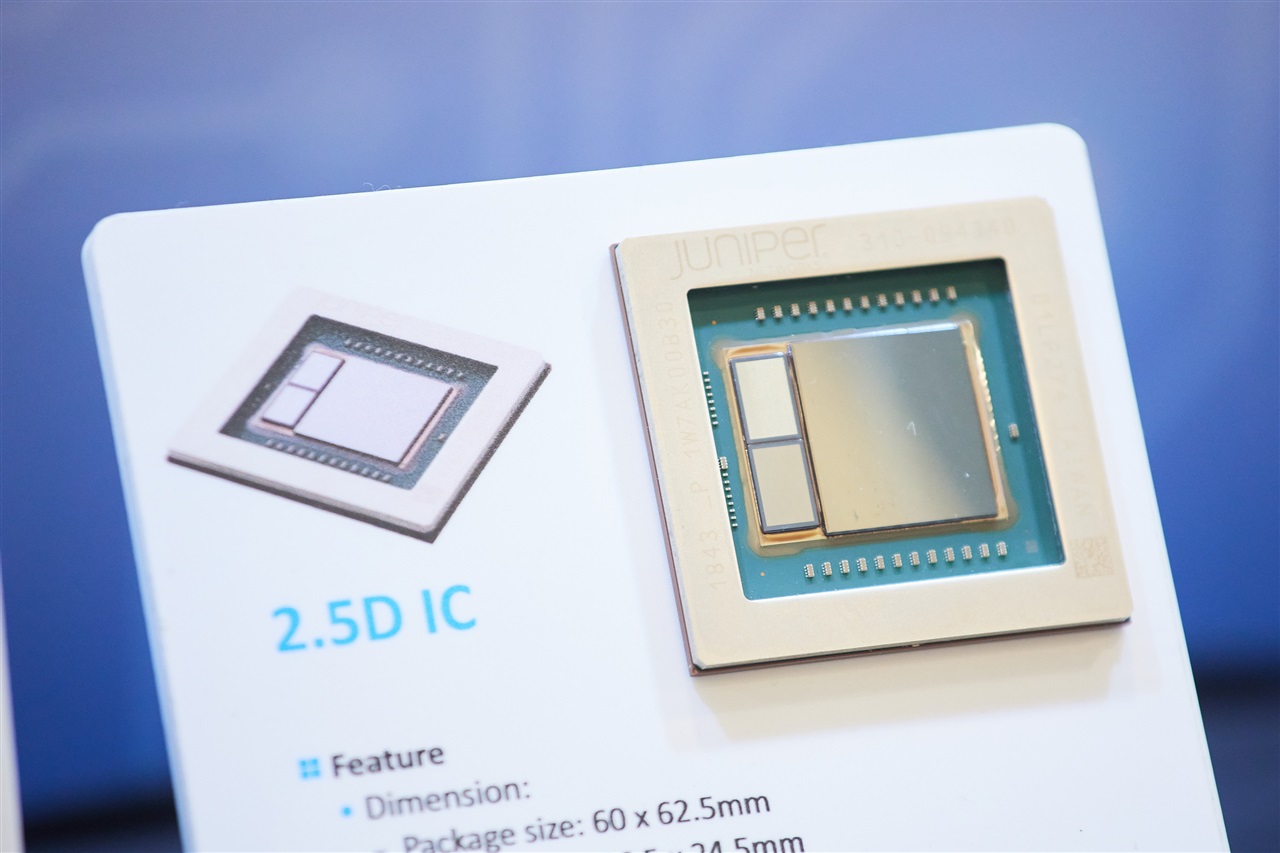

For those evaluating on-premise deployment of Large Language Models, the names of OSAT companies reveal as much as the specifications of a GPU or an accelerator. Advanced packaging — the techniques that stack chiplets, bring memory closer to logic, and manage extreme thermal densities — has become the critical bottleneck for large-scale inference. Technologies like TSMC's CoWoS (Chip-on-Wafer-on-Substrate) or Intel's EMIB depend not only on foundries but also on packaging and testing subcontractors. A broader production base, with the entry of credible new competitors, could erode the incumbents' bargaining power and reduce hardware lead times.

That a small company is gaining attention suggests at least three possible developments. First, it may have developed a specialization in AI chip packaging — for instance, organic interposers or hybrid solutions for HBM memory — carving out a profitable niche. Second, the market could reward those offering regional alternatives: for a European organization that must comply with data residency requirements and prefers less geographically concentrated supply chains, a more distributed packaging ecosystem lowers systemic risk. Third, the impact on pricing: more qualified suppliers mean better negotiation margins, directly influencing the Total Cost of Ownership of an on-premise cluster.

It's no coincidence that the OSAT sector is experiencing upheaval. As inference demand keeps climbing, chiplet architectures become the norm for scaling beyond reticle limits. Companies like AMD, NVIDIA, and the big hyperscalers design custom silicon that then must be assembled and tested, fueling a market worth tens of billions. The rise of a new player, however small for now, forces a rethinking of technological dependency maps.

For those currently assembling computing infrastructure for self-hosted LLMs, the message is clear: tracking GPU roadmaps alone isn't enough. The variables that determine a project's feasibility — from compute power to memory latency and energy costs — are shaped upstream, inside packaging facilities. A more contestable sector can accelerate on-premise adoption and give system integrators an extra lever to design truly sovereign architectures.

💬 Comments (0)

🔒 Log in or register to comment on articles.

No comments yet. Be the first to comment!