The bare news comes from agencies: China's chip supply chain is under pressure, from AI server MLCCs to 8-bit MCUs. The detail, seemingly technical, carries strategic weight for those planning local computing infrastructures.

Invisible components, real bottlenecks

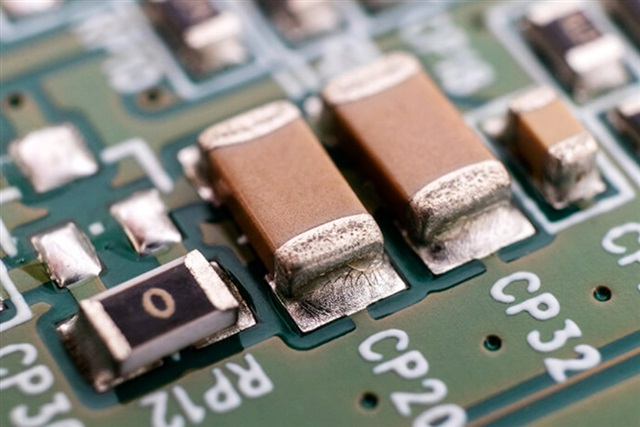

MLCCs are essential passive components in any high-density board. In servers handling LLM inference and training, they manage power decoupling, transient regulation, and signal integrity among GPUs, VRAM, and interconnects. A single AI server may require thousands of them. When supply tightens – and Chinese factories face mounting pressure on raw materials and production capacity – entire assembly lines slow down.

8-bit microcontrollers, often overlooked as commodities, govern power delivery, thermal sensors, and control modules in server nodes. Their unavailability blocks production just as effectively as more iconic components.

On-prem LLMs: hardware that won’t arrive

Self-hosted LLM deployment – whether for data sovereignty, regulatory mandates like GDPR, or multi-year TCO calculations – relies on servers equipped with GPUs featuring ample VRAM, high memory bandwidth, and advanced cooling architectures. Lead times are lengthening, prices are climbing, and delivery uncertainty complicates cluster sizing. Those who were evaluating next-gen GPU configurations might have to fall back on lower-spec models, sacrificing inference capacity.

AI-RADAR analysis: counting every piece of the puzzle

In the analytical frameworks we apply – and that we help build on this publication – the Total Cost of Ownership of an on-prem installation cannot be limited to GPU costs. Procuring passive components, control subsystems, and even cooling mechanics affects initial CapEx and operational OpEx. The Chinese squeeze is a signal: the AI hardware value chain is fragile if measured only by advanced silicon production capacity. It extends to ceramic materials, discrete semiconductor silicon, and packaging.

For those choosing between on-prem, hybrid cloud, or fully managed, the current environment forces the inclusion of supply risk metrics in their plans. This is not a temporary hiccup but a structural feature of an ecosystem where roughly 70% of passive components originate from East Asia.

Outlook: rethinking procurement without losing control

The contraction in MLCC and MCU availability is not a temporary stumble; it’s a symptom of a supply system that needs diversification. Companies pushing for on-prem find value in strategic stockpiling, exploring non-Chinese suppliers, or accepting price premiums to retain infrastructure sovereignty. The trade-off remains: move everything to the cloud? Not if it means giving up data control and marginal inference costs. But the implementation plan must be robust, and today it hinges even on components as small as a grain of sand.

💬 Comments (0)

🔒 Log in or register to comment on articles.

No comments yet. Be the first to comment!