The Genesis of Ramageddon: A Structural Reallocation of Silicon

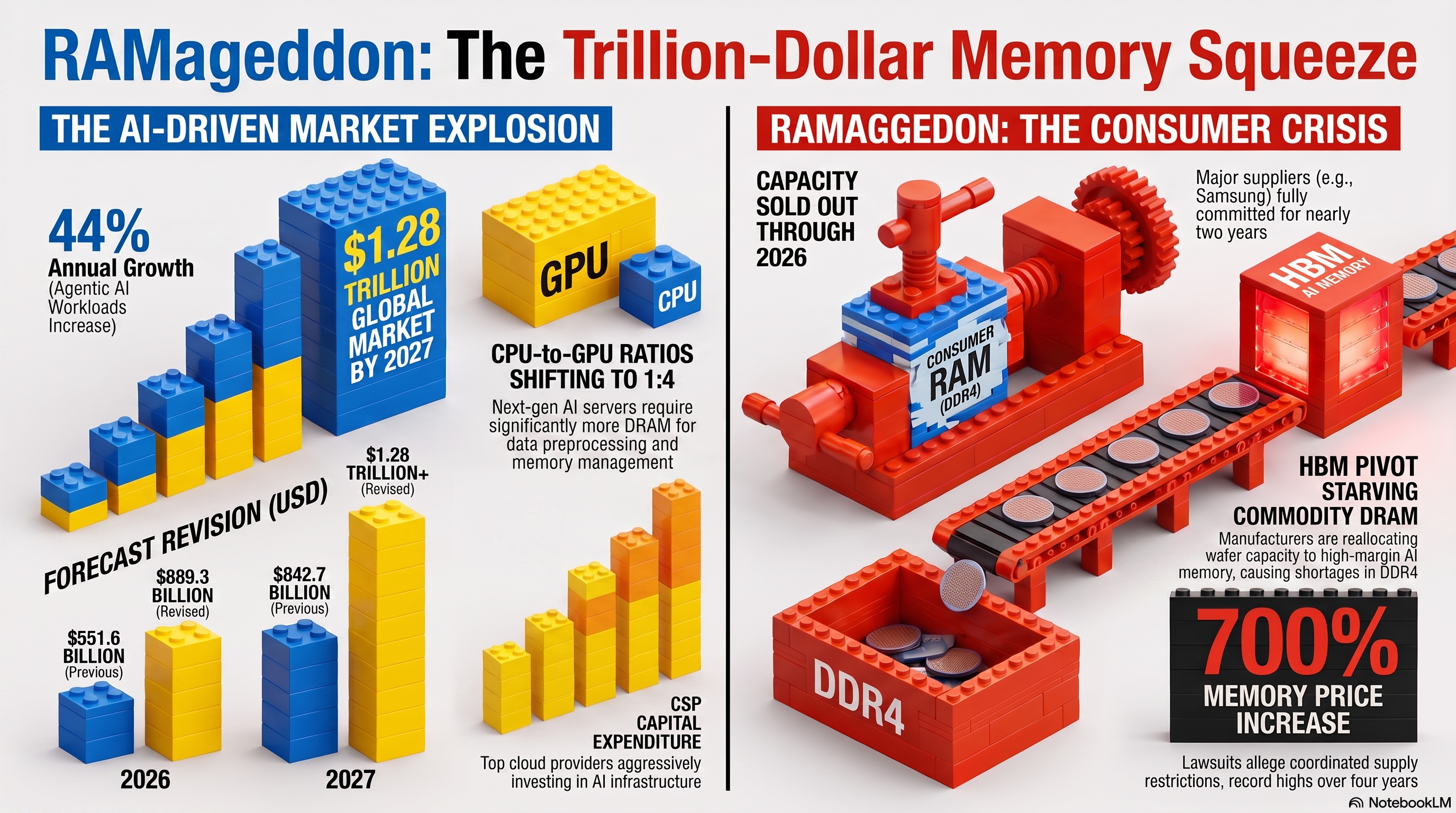

The global semiconductor ecosystem is currently enduring an unprecedented structural supply deficit and a hyper-inflationary pricing wave, a phenomenon industry analysts and technology executives have officially dubbed "Ramageddon". At the heart of this crisis is a massive and highly asymmetric reallocation of manufacturing capacity by the world's three dominant memory manufacturers—Samsung Electronics, SK Hynix, and Micron Technology. These three firms, which collectively control over 90% of global dynamic random-access memory (DRAM) revenue, have aggressively diverted their cleanroom space and capital expenditures away from conventional consumer memory and toward High-Bandwidth Memory (HBM) and server-grade DDR5 modules to satisfy the insatiable needs of artificial intelligence (AI) data centers.

This transition has created a zero-sum game within semiconductor fabrication plants. Every silicon wafer allocated to complex HBM stacks for AI servers is a wafer denied to the LPDDR5X modules of smartphones or the solid-state drives (SSDs) of consumer laptops. Data centers are forecast to consume 70% of all memory chips produced worldwide in 2026, a staggering shift from the 20% to 30% they accounted for in 2022. As a result, the technology sector is facing the most severe memory supply crunch in modern history.

The Forecasts: A Hyper-Inflationary Super-Cycle

The financial forecasts surrounding this memory crisis point to a super-cycle of explosive revenue growth and punishing component inflation. TrendForce has drastically revised its global memory market projections, estimating the market will reach $889.3 billion in 2026 before surging past $1.28 trillion by 2027—an annual growth rate of approximately 44%. DRAM revenue alone is projected to hit $618.7 billion in 2026, representing a 303% annual increase.

This revenue explosion is driven entirely by skyrocketing prices. Contract prices for DRAM surged by an estimated 90% to 95% quarter-over-quarter in the first quarter of 2026, and an additional 58% to 63% in the second quarter. In the retail spot markets, general-purpose NAND flash surged more than fivefold in just six months, rising from $5.70 at the end of 2025 to $28.80 by mid-2026.

The cost of next-generation HBM4 is poised to break industry records. While HBM currently sits at roughly $16.60 per gigabyte (GB), investment bank Bernstein forecasts that HBM4 prices will triple to $53 per GB in 2027 as Nvidia's Vera Rubin AI chips begin shipping in volume. Standard HBM contract prices are projected to rise by a factor of 2 to 2.5 times next year as memory suppliers attempt to close the widening profitability gap between HBM and conventional DRAM, which has already increased by 4.5 times in recent quarters.

| Market Metric | 2025 Baseline | 2026 Projection | 2027 Forecast | Growth / Multiplier |

|---|---|---|---|---|

| Global Memory Revenue | $551.6 Billion (Prev. Est) | $889.3 Billion | $1.28+ Trillion | +44% YoY (2027) |

| Global DRAM Revenue | ~$153.5 Billion | $618.7 Billion | $903.3 Billion | +303% YoY (2026) |

| NAND Flash Revenue | ~$71.2 Billion | $270.6 Billion | $379.4 Billion | +280.7% YoY (2026) |

| NAND MLC Flash (128Gb) | $5.70 per unit | $28.80 per unit | N/A | 5.05x Increase (6 Months) |

| HBM4 Contract Price | $16.60 per GB | N/A | $53.00 per GB | 3.19x Price Surge |

| Table 1: Memory Market Revenue and Price Projections. | ||||

Is It Going to Last? The Anatomy of a Structural Deficit

The prevailing consensus among industry analysts and executives is that Ramageddon is not a brief, cyclical supply-demand mismatch, but a long-term structural deficit. SK Group chairman Chey Tae-won has bluntly warned that the memory chip shortage will likely last until 2030.

The core issue lies in the physical and operational inefficiency of manufacturing High-Bandwidth Memory. Producing HBM requires up to four times the wafer area of conventional DRAM of equivalent capacity, and the manufacturing process suffers from significant yield losses due to the complexity of high-stack 12-layer assembly. TrendForce estimates that by the end of 2027, HBM wafer inputs will account for 30% of total global DRAM wafer starts, yet due to these inefficiencies, it will only yield 13% of the total DRAM bit supply. This Capacity Efficiency Ratio guarantees that conventional DRAM output will remain structurally depressed.

Compounding this deficit is the aggressive procurement strategy of hyperscale cloud service providers (CSPs) like Microsoft, Meta, Google, and Amazon. These tech giants have insulated their AI infrastructure roadmaps by locking up the vast majority of global DRAM wafer starts through three-to-five-year Long-Term Agreements (LTAs). Micron has finalized over $100 billion in such long-term supply commitments, and SK Hynix announced that it had sold out its entire 2026 capacity for HBM, DRAM, and NAND by October 2025. By 2027, it is estimated that nearly half of all global DRAM production capacity will be completely unavailable to mid-sized and smaller hardware manufacturers. While new fabrication plants are under construction—including Micron's $150 billion mega-fab initiatives in the United States—meaningful incremental DRAM output from these facilities is not expected until late 2027 or 2028.

A Hidden Cartel? The Antitrust Allegations

As the global supply chain fractures, a massive legal battle has emerged to question the true nature of this shortage. On June 25, 2026, a class-action lawsuit, Garciaguirre et al v. Samsung Electronics Co., Ltd. et al, was filed in the U.S. District Court for the Northern District of California. The lawsuit accuses the "DRAM Triarchy"—Samsung, SK Hynix, and Micron—of running a coordinated scheme to artificially restrict supply and inflate prices, violating Section 1 of the Sherman Antitrust Act.

The plaintiffs allege that these three companies used the industry's pivot to HBM as a convenient cover to deliberately curtail the production of commodity DDR3 and DDR4 memory, starving the consumer PC and smartphone markets to drive up prices by roughly 700% over a four-year period. To prove an illegal conspiracy rather than lawful "conscious parallelism," the plaintiffs have cited several suspicious "plus factors". These include near-simultaneous production cuts announced by all three firms in late 2022 despite a severe memory downturn, a synchronized customer-vetting regime purportedly used to jointly monitor supply, and Micron's abrupt decision to shut down its profitable consumer-facing Crucial memory brand.

What gives the lawsuit distinct gravity is the historical track record of the defendants. Between 1998 and 2002, Samsung, Hynix, and Micron operated a proven, criminal DRAM price-fixing cartel. The U.S. Department of Justice extracted guilty pleas from Samsung and Hynix, resulting in over $730 million in criminal fines and prison sentences for executives, while Micron avoided fines only by turning whistleblower under a corporate leniency program. While a similar lawsuit covering the 2016-2017 memory super-cycle was dismissed in 2020 by federal courts, the plaintiffs in the 2026 case believe the coordinated HBM transition provides the necessary evidence of an actual, illegal agreement.

If the lawsuit survives motions to dismiss and enters discovery, the three manufacturers will be forced to expose their internal communications regarding HBM allocations, presenting a monumental risk to their current record-breaking profit margins.

The Escalating Toll on AI Infrastructure Costs

Will this memory crisis negatively impact AI costs even more? Yes, to an exponential degree. The physical limitations of monolithic silicon have forced chip designers to adopt multi-chip module (MCM) designs, fundamentally altering the economics of advanced processors. Historically, the logic die was the most expensive part of a chip; today, HBM and advanced packaging have overtaken it.

On an Nvidia Blackwell B200 accelerator, the logic dies cost approximately $850—representing only 13% of the total manufacturing cost. By contrast, the 192GB of HBM3e memory costs roughly $2,900, accounting for 45% of the total bill of materials (BOM).

| Accelerator Model | GPU/ASIC Vendor | Logic Die Cost | HBM Memory Cost | Packaging Cost | Total Est. COGS | Est. Selling Price |

|---|---|---|---|---|---|---|

| H100 SXM5 | NVIDIA | $300 | $1,350 (80GB) | $750 | $3,320 | $28,000 |

| Blackwell B200 | NVIDIA | $850 | $2,900 (192GB) | $1,100 | $6,400 | $40,000 |

| GB200 Superchip | NVIDIA | $1,700 | $5,800 (384GB) | $2,200 | $13,500 | $65,000 |

| Instinct MI300X | AMD | $600 | $2,900 (192GB) | $1,200 | $5,300 | $15,000 |

| Gaudi 3 | Intel | $1,500 | $1,950 (128GB) | $1,200 | $6,500 | $15,625 |

| Table 2: AI Accelerator Manufacturing Cost Breakdown. | ||||||

The commercial impact of this memory inflation is heavily magnified by the pricing strategies of GPU suppliers through what analysts call the "Markup Multiplier". Because HBM is packaged inside the GPU, it is treated as part of the raw COGS. To preserve its industry-leading 75% gross margins, a company like Nvidia must increase the retail price of its hardware by four times the amount of any raw component cost increase. Therefore, a $100 increase in HBM manufacturing costs forces a $400 increase in the final GPU price.

When extrapolated to rack-scale systems, the financial burden becomes staggering. Bernstein analysts estimate that Nvidia's next-generation Vera Rubin (VR200) NVL72 rack will cost approximately $9.09 million. Of that figure, memory and storage components alone will account for $3.2 million, driven by $1.09 million for HBM4, $800,000 for LPDDR5X system memory, and $1.28 million for enterprise flash storage. The Rubin Ultra V300 "Kyber" racks are expected to push the boundaries of capital expenditure even further, carrying an estimated price tag of $21 million, with $1.534 million dedicated solely to HBM4e memory.

| System Architecture | Compute Hardware | Memory & Storage Cost (Per Rack) | ASP / Rack | Capital Intensity (Per GW) |

|---|---|---|---|---|

| Blackwell NVL72 | 72x B200 GPUs + 36x Grace CPUs | ~$600,000 | ~$3.0 Million | ~$40.5 Billion |

| Vera Rubin NVL72 | 72x V200 GPUs + 36x Vera CPUs | $3,200,000 (Bernstein Est.) | $9.09 Million | ~$47.3 Billion |

| Rubin Ultra NVL144 | 144x V300 GPUs | $1,534,000 (HBM4e only) | $21.0 Million | ~$47.3 Billion |

| Table 3: Rack-Scale System Economics. | ||||

At a data center scale, building a 1-gigawatt AI facility deploying Vera Rubin racks will require an estimated $47.3 billion in capital expenditures, a significant leap from the $40.5 billion required during the Blackwell cycle. Bernstein forecasts that hyperscale cloud providers will be forced to raise their overall AI capital expenditures by approximately 30% simply to absorb these escalating memory costs.

Consequently, CSPs are engaged in a rapid "cost rebalancing," altering how cloud compute is priced for developers. While an Nvidia H100 can be rented for $2.00 per hour, a GB200 NVL72 costs $8.00 per hour. Because the industry is shifting toward "Agentic AI"—which requires continuous, iterative reasoning and massive key-value (KV) caches—memory bandwidth and capacity have become the ultimate bottlenecks. End-users requiring large context windows will be forced onto higher-tier API plans, meaning the exorbitant costs of the memory shortage will be transferred directly to consumer and enterprise software applications.

The Crushing Weight on Consumer Electronics

While data centers fight over advanced memory, the consumer electronics market is being decimated. PC manufacturers like HP report that memory now accounts for 35% of a computer's bill of materials, up drastically from historical norms of 15% to 18%. Without the massive purchasing power of the hyperscalers, smaller device makers are facing an "absolute existential crisis".

To survive, manufacturers are passing the costs onto consumers. Apple has hiked prices across its MacBook and iPad lineups, with the base MacBook Pro jumping by $300 to $1,999. Microsoft increased Xbox console prices by up to $150, openly citing memory costs that have more than doubled and are expected to double again by 2027. Sony raised PlayStation 5 prices years after its initial launch, and Valve's new Steam Machine is launching at over $1,000 due to non-negotiable memory pricing.

For budget buyers, the outlook is bleak. Market analysts project that sub-$500 entry-level laptops will entirely disappear from the market by 2028 because vendors can no longer absorb the component costs. Smartphone makers are quietly freezing RAM specifications at 12GB instead of upgrading to 16GB, or deliberately shipping devices with less memory than previous generations at equal or higher price points.

Conclusion

Ramageddon is not a temporary supply chain glitch; it is a fundamental rewiring of the global technology economy. Samsung, SK Hynix, and Micron have successfully transformed memory chips from a cyclical commodity into a macro-economic weapon, extracting unparalleled wealth from the artificial intelligence gold rush. Whether orchestrated through an illegal cartel or born from the sheer gravitational pull of hyperscaler debt-spending, the result is undeniable: the cost of participating in the digital future has skyrocketed, and from the largest AI data center down to the cheapest budget smartphone, everyone is paying the price.

💬 Comments (0)

🔒 Log in or register to comment on articles.

No comments yet. Be the first to comment!